The preliminary investment volumes for the CEE region for Q1 2020 have reached ca. €3.7 billion, despite the onset of COVID-19 in CEE at the beginning of March. This volume was significantly boosted by the ca. €1.3 billion acquisition of the Residomo portfolio in the Czech Republic by Heimstaden, however, it still represents a y-o-y growth of 68% over Q1 2019 (ca. €2.2 billion) and 28% over Q1 2018 (ca. €2.9 billion).

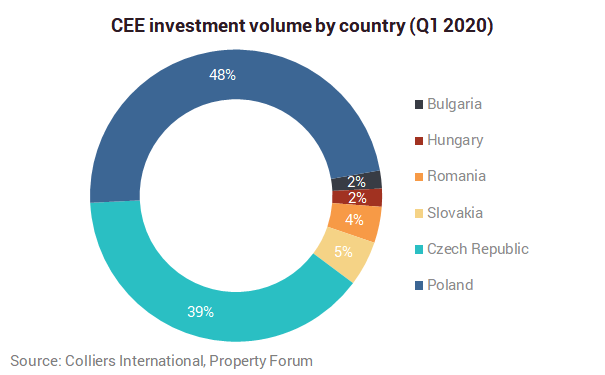

After a record-breaking year in 2019, Poland maintains its leading position in the region with a 48% share of the Q1 volume, followed by Czech Republic (39%), Slovakia (5%), Romania (4%), Hungary (2%) and Bulgaria (2%).

Kevin Turpin, Regional Director of Research | CEE adds: “Due to the various measures imposed to keep people safe and prevent the spread of the virus, including flights and border restrictions, we expect that the volumes in Q2 and Q3 will be significantly impacted as all parties involved in transaction processes are largely unable to meet or visit properties.”

In addition to these hopefully fairly short term restrictions, many property owners and managers are currently busy assessing and managing any risks to their assets. Individual responses to the pandemic by the region’s governments have, to date, mainly been focused on addressing the salaries of employees and supporting businesses, particularly those most impacted by the restrictive measures. Other than some potential short term tax relief, many property owners may well feel left out when it comes to the protective measures.

According to initial results from an ongoing Colliers survey, investor appetite remains strong, the volume of capital for deployment also remains and could potentially increase, but many investors will hold off on decisions for a number of weeks until the situation becomes clearer, particularly in regard to financing, pricing and the ability to physically view potential opportunities.

All of the above outlooks are subject to how long the pandemic will continue to impact on our lives, to what extent of damage is caused economically and how all active players can recover and adapt to the changes that will certainly come, or at least remain in the short to mid-term future. After all, whether you are a developer, bank, investor, occupier or advisor, there will be an impact for all.