2016’s record-breaking €12.2 billion investment in the real estate sector in the CEE region is likely to be surpassed in 2017 – this is according to CEE Real Estate Investment Compass 2017 published by Colliers International and CMS. The sources of investment flows into the CEE region are also expected to remain diverse in 2017, with Asian and CEE investors becoming increasingly active in the real estate market.

The CEE Real Estate Investment Compass 2017 examines key trends in the real estate markets of six of the region’s countries (Bulgaria, Czech Republic, Hungary, Poland, Slovakia and Romania) over the last five years, and takes a look at what is on the horizon for 2017.

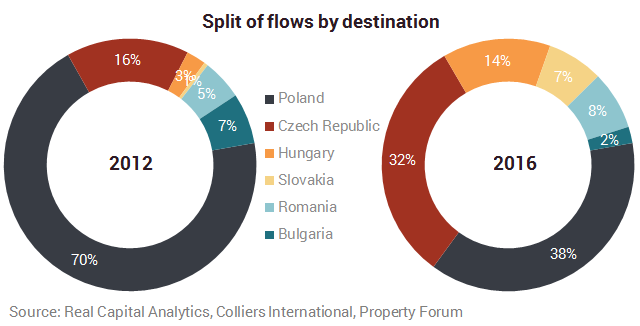

In the first quarter of 2017, preliminary real estate investment in the CEE-6 markets stood at €2.3 billion, representing a 41% increase compared to Q1 2016. The region has started the year well. Of that, the Czech Republic received 62% of the total real estate investment in CEE during the period at €1.4 billion.

“The growing maturity of the CEE region may help combat the specific risks affecting Western Europe, that of ‘Brexit’ and its reverberations, which may unfold further in 2017. Brexit’s full consequences are not yet known and some might even end up as a positive for CEE,” says Mark Robinson, senior researcher, CEE, Colliers.

"After a solid 2016, the Czech Republic experienced a particularly buoyant first quarter in which it received over 60% of the overall real estate investment across the region. The short to midterm market performance could be affected by the CNB’s exit from the Czech Crown intervention regime,” comments Lukas Hejduk, head of CMS’ Czech and Slovak real estate practices. “The Slovak market continues to perform on a healthy and stable level with promising opportunities for new projects."

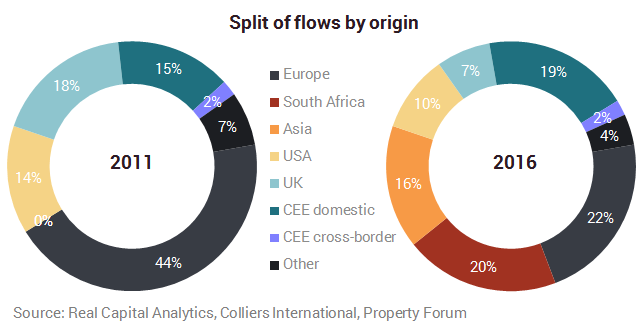

The report identified a marked shift in the origin of flows to CEE in 2016 compared to previous periods in this cycle. South Africa, Asia and flows from domestic/CEE sources are now larger than those from G10 countries. Preliminary indications from Q1 2017 suggest continued significant local investor activity in Hungary and the Czech Republic, as well as the entry of Thai investors into Hungary and Poland.

“The total investment activity in 2016 and the volume of completed deals in Q1 2017 drives the sense of optimism going ahead and 2017 may very well be the strongest year ever in the history of the Hungarian capital markets. The level of oversubscription of transactions and the improving pricing effect of strong commercial property fundamentals will be evidenced in the growing transaction volume. Further, we expect to register new markets entrants in 2017 and 2018.” – commented Bence Vecsey, Head of Investment Services at Colliers International Hungary.

Looking at trends in 2017 in the CEE region, increased returns via lower yields are predicted in Budapest and Bucharest (office, retail and industrial), and in Prague (office and industrial), while in Bratislava (all sectors), Warsaw (industrial and retail) and Sofia (office and industrial) a similar market situation is expected.

Looking at the various segments, the share of office transactions in the CEE investment pie has remained broadly steady around the 40% mark (39% in 2016), while the absolute value of transactions has, of course, grown. The most impressive increases seen in the last year were in the Czech Republic (€1.7 billion in 2016 versus €556 million in 2015) and Hungary (€939 million versus €291 million).

As the most liquid investment asset class, office yields have compressed along with funding rates in this cycle, and the authors of the report foresee some chance of further yield compression in prime Prague, Budapest and Bucharest given the investment demand and rent growth dynamics.

CEE retail has been a clear story of firming rental dynamics, mostly because out of all the key real estate sectors it has the clearest positive link to consumer demand and wage growth. More money in the pockets of employed consumers, including many benefiting from significant hikes in the minimum wage in the likes of Hungary (30% over 2 years), Romania (16%) and the Czech Republic (11% in 2017), will translate into higher spending on both staples and discretionary goods. In the Czech Republic specifically, the probable appreciation of the Czech Koruna after the “currency cap” was removed by the central bank at the beginning of April 2017 will increase the purchasing power of Czech consumers further.

The CEE industrial sector is also booming, with a bright start to 2017 already recorded in official economic figures. For both manufacturing and logistics, wage pressures are the main macro risk to consider in the near term, with data from the quarterly industrial sentiment surveys collected by the European Commission suggesting that 33% of Czech companies and 22% of Slovak companies seeing a shortage of labour as a constriction on expanding production. The highest ratio in the region was Hungary at more than 75%.