Cushman & Wakefield has published its new CE industrial map to give a comprehensive overview of the most important logistics and industrial sites in Central Europe, Russia and Germany. In addition, this year’s edition has been expanded with figures for Italy’s Milan.

Ferdinand Hlobil, Head of Cushman & Wakefield’s CE Industrial Team, said: “A comparison of the current and previous maps gives us interesting insights into market trends. New parks have been built in almost all locations but the vacancy ratio has decreased significantly. Central Europe is beginning to experience a shortage of available space to lease – which may lead manufacturing companies to look at other locations. For example, Spain or Portugal might become our competitors.”

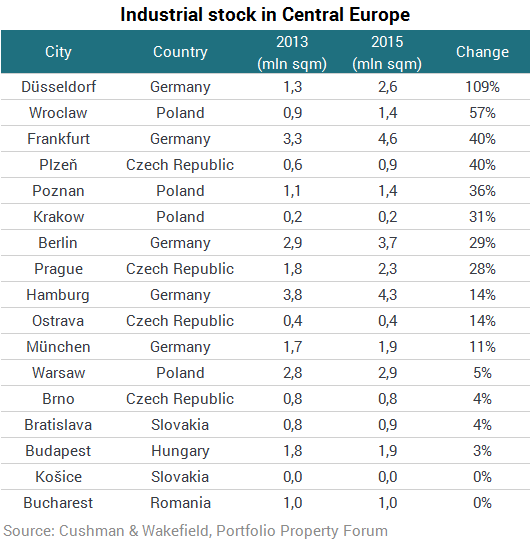

Between the end of 2013, when the last map was produced, and the start of 2016 the total area of industrial units across Central Europe (the Czech Republic, Hungary, Poland, Romania and Slovakia) grew by 25% from approximately 16 million to 20 million square metres. The greatest amount of existing stock is currently in Warsaw (almost 3 million sq m), Prague (2.3 million sq m) and Budapest (1.9 million sq m).

Cushman & Wakefield forecasts that new developments are set to markedly decrease in Prague over next few years due to a shortage of available land. Conversely, significant potential for new development can be seen e.g. in Warsaw region (approx. 0.3 million sq m), Poznan and Central Poland (approx. 0.25 million sq m each).

Mr Hlobil said: “Our occupancy statistics indicate that the vacancy rate has dropped by more than 50% in many locations including Cracow, Bucharest, Poznan and Budapest. One could say that there is currently almost no vacant space available for immediate lease in Cracow and Poznan. Companies intending to expand into those areas will have to wait for new development.”

The situation is different in Russia where the economic slowdown is reflected in the industrial property market. As a result of subdued consumer demand, companies are not extending their leases. As a consequence, the ratio of vacant space is growing even though recent development has been low.

However, Mr Hlobil added: “This situation is unique to the Russian market and Central Europe is experiencing a period of growth that we expect to continue for the foreseeable future.”