A joint initiative by the Magyar Nemzeti Bank (The Central Bank of Hungary – MNB) and the Royal Institution of Chartered Surveyors (RICS), the Market Sentiment Survey, a questionnaire-based survey looking at the developments of the Budapest commercial property market, was recently relaunched for the second half of 2017. The common objective of MNB and RICS is to increase knowledge and consciousness regarding commercial property market developments and improve market transparency.

The Market Sentiment Survey monitors market sentiment on a bi-annual basis on the Budapest commercial property market. Respondents provide data on the typical rents, lease periods and yields of the various segments (offices, industrial and logistics, retails, hotels). Furthermore, in connection with the market developments for the period under review and real estate experts’ market expectations for the next 6 months, the survey includes questions related to changing trends in investor and occupier demand and development activity.

Surveys between 2011 and 2015 were conducted jointly by RICS, Portfolio.hu and ELTINGA Centre for Real Estate Research. Market Sentiment Survey data for the period between 2011 and 2015 included in this Press Release were processed by ELTINGA.

The survey relaunched by MNB and RICS for the second half of 2017 involved 43 experts and it is expected that the number of participants will increase in the future. Among respondents, consultants (42 percent) and property development experts (30 percent) were in the majority (Chart 1). 51 percent of respondents work for local companies while 49 percent for internationally active companies.

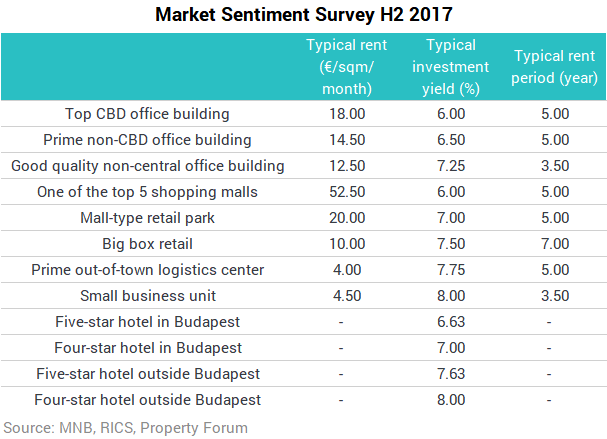

Since the latest survey covering the second half of 2015, the typical rent for commercial properties observed for most property types has increased by more than 15 percent until the end of the second half of 2017 (Chart 2). Based on the reports published by international property consultants, the highest possible rent (prime ) achievable in Budapest may well increase by a further 20-30 percent, compared to the rent of a Top CBD office calculated from the answers given in the survey.

Compared to the results of the previous survey for the second half of 2015, typical yields significantly decreased in every segment (Chart 3). Prime yields for the office market and shopping centres approached the historical minimum observed in 2007 with 10-25 basis points.

The majority of respondents expect a growth in the demand for investment in the next 6 months, especially in the office market. An increase is expected mainly for properties of the best quality and location which mean lower risks and yields for investors.

Projections are more balanced when assessing development activity. The unchanged development activity in the retail segment may be explained by the existing regulations, according to which obtaining a building permit for a commercial establishment with an area exceeding 400 square meters requires a specialist authority procedure. Although the office market is already witnessing a large volume of ongoing developments, the majority of respondents expect a further increase in development activity. The opinion of survey participants anticipating an unchanged market in respect of the industrial-logistics segment may reflect a shortage of development plots at appropriate prices and locations, as market fundamentals (demand, vacancy rates, rents) would otherwise justify an increase. This discrepancy might be improved by developing rail and road infrastructures – in addition to the already announced projects – in the future.

Market participants forecast strong occupier demand for each property type, especially for properties of the best quality and location, in particular for Top CBD offices and Prime non-CBD offices.