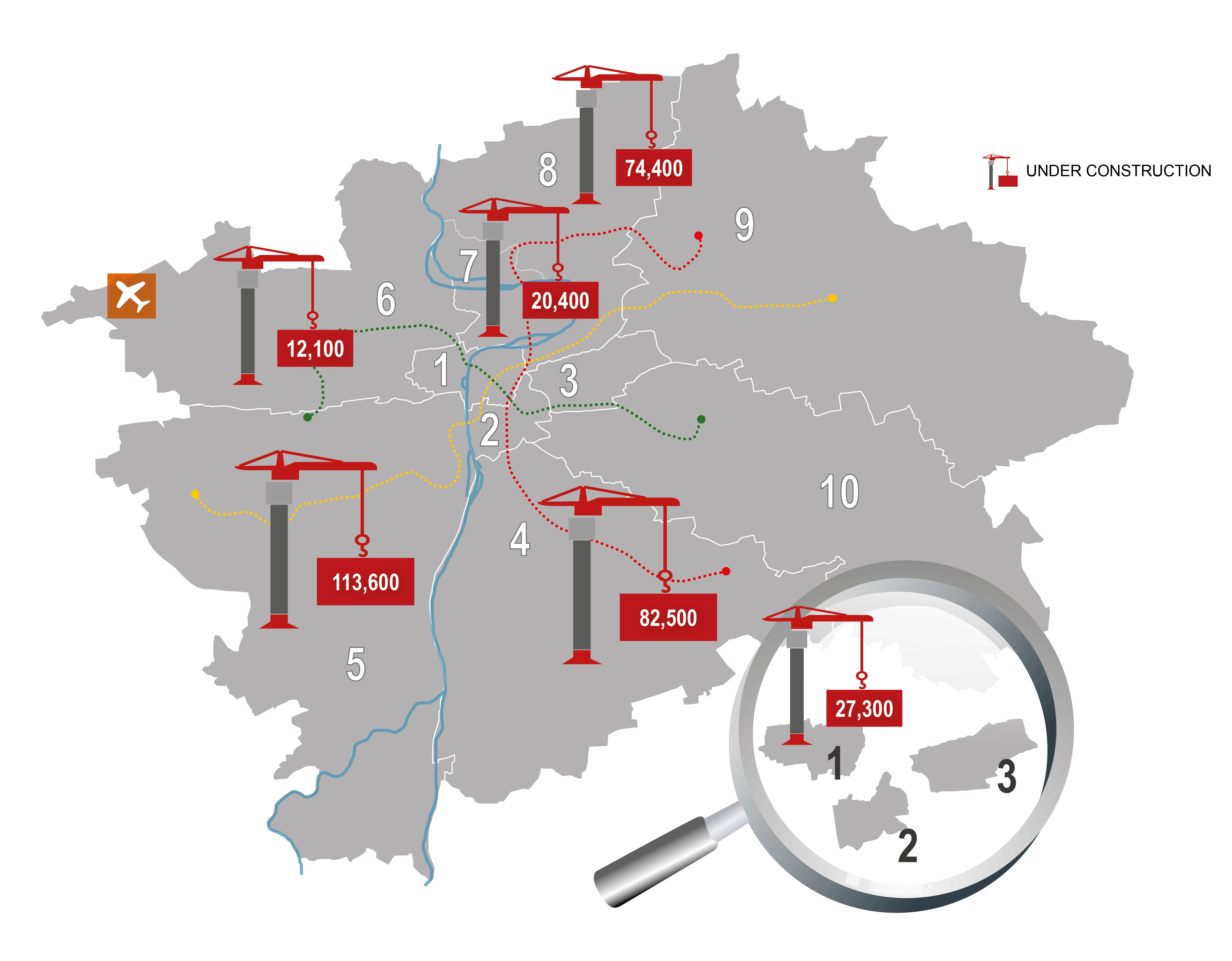

Office tenants can look forward to a new supply of administrative space that is going to be delivered to the Prague market in 2017 and 2018. Last´s year paradox, when the economy was booming and the market registered a robust demand for new office space, but the amount of new completions dropped to a historical low, is forecast to be cleared out in the months to come. Currently, there are 330 000 sqm of new offices under construction in Prague out of which approximately half (171 000 sqm) is expected to be delivered this year. JLL looked at the largest office submarkets of the Czech capital in detail.

With its 26.8% share of the total stock, Prague 4 forms the largest office district in Prague. Prague 4 is characterised by several large scale developments such as unique projects as The Park, BB Centrum or the intensively developed area around the Pankrác metro station. Currently, there are 82 500 sqm within 5 office schemes being developed in Prague 4 which are expected to be completed within the next 2 years. The largest are Main Point Pankrác (24 000 sqm), the complete refurbishment of two buildings of BB Centrum (A – 21 400 sqm and C – 11 600 sqm) and Trimaran / City Deco (18 300 sqm). The Pankrác Prime (7 000 sqm) close to the Pražského povstání metro station provides an interesting alternative for tenants who appreciate smaller scale projects.

Prague 5

The largest amount of new office premises (113 600 sqm) is currently being developed in Prague 5 which has got 16.2% market share of the total stock and therefore is the second largest office district in the Czech capital. A few schemes are intensively developed around Radlická metro station such as it the second headquarters of ČSOB bank (30 000 sqm) or new buildings of the Waltrovka office complex (buildings such as Mechanica 31 100 sqm or Dynamica 13 400 sqm). The Mechanica´s pre-lease of 15 000 sqm to Johnson & Johnson is a big success of Waltrovka´s developer Penta. An interesting microlocation in Prague 5 is the Smíchovské nádraží railway station where Skanska Commercial Development is preparing Five office building which has been pre-leased (11 300 sqm) to MSD, a pharmaceutical company.

Prague 1

Prague 1, with its 15.8% market share of the total stock the third largest office district, is going to provide the tenants with 27 300 sqm of new office space. With respect to the historical centre of Prague, the new office schemes are of smaller scale. There are 5 projects under construction – a newly built Palác Národní and 4 complete reconstructions (Šporkovský palác and buildings Albatros, Mango and Omnipol). Šporkovský palác, developed by Sebre, can also boast preleases signed for 80% of the total premises, after its completion, it is to become a seat of a prestigious law firm.