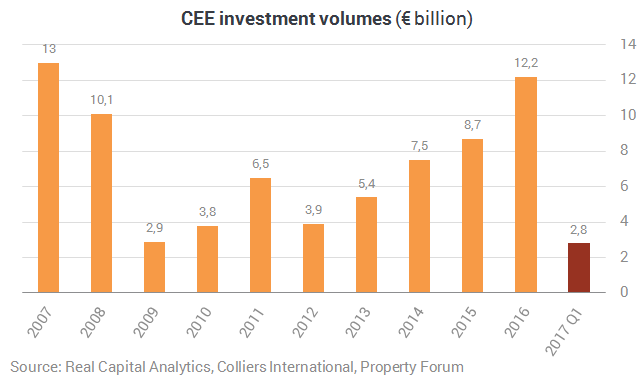

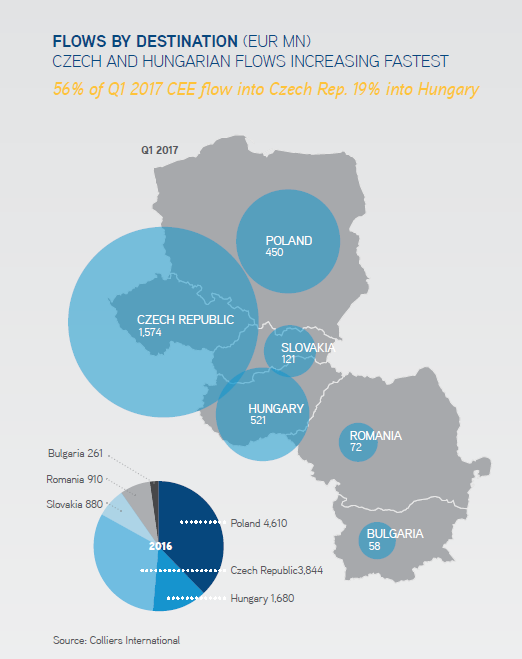

Investment flows into the CEE region rose 70% year-on-year in Q1 2017. The level of €2.8 billion is some €0.5 billion higher than the preliminary estimate of €2.3 billion Colliers International published at the beginning of April. Money invested into the Czech Republic (56% share) and Hungary (19% share) contributed particularly to the significant jump. Looking within the numbers, the retail sector accounted for nearly half (47%) of the flows, leaving the office sector trailing with a 21% share. Of interest and also a sign of buoyant economic growth, the fastest growth was seen in the hotel sector with a portfolio transaction contributing to the €415mn total (a 15% share).

Assessing the origin of funds, Collier noted in its March research, continued in one vein in the first quarter, with domestic CEE flows amounting to 27% of the overall total, with another 18% of the pool of money flowing cross-border in CEE.