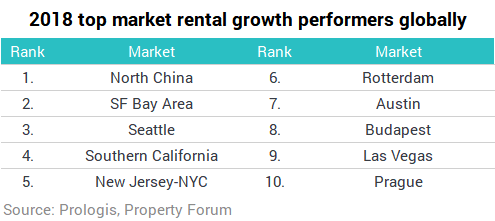

Logistics real estate rent growth remained considerable in 2018, with rents rising 6% globally. Consistent with the past several years, the U.S. outperformed, with 8% growth. However, other regions were just as notable. China was a clear leader with 8% growth. In Europe, rents rose 5%, a near doubling in growth from 2017 and the fastest annual growth in the region based on data reaching back more than 10 years, according to new research by Prologis.

Why does it matter?

- Pricing is historically strong, with low vacancies translating to higher rental rates as customers compete for available space.

- High-barrier-to-supply markets with geographic, legislative and other hurdles to new development have the strongest fundamentals.

- Customers who plan well and can act quickly will secure the best space in an increasingly competitive environment.

What’s next?

- Despite recent macro volatility, market vacancy rates are at or near historic lows, leading users to bid rents higher in pursuit of their needs.

- New construction costs are growing at a historically high pace, prompting mid- to high-single-digit annual growth with leading markets well into the double digits.

- Strengthening conditions in Europe are expected to shift growth leadership towards the region.

Global overview

The Prologis Logistics Rent Index, introduced in 2015, examines trends in net effective market rental growth in key logistics real estate markets in the United States, Europe, Asia and Latin America. Prologis’ methodology focuses on taking rents, net of concessions, for logistics facilities. Prologis Research combines local insight on market pricing with data from its global portfolio to produce the index.

Key findings:

- Rent growth remains high. Rents grew 6% in 2018, in keeping with similar growth in 2017.

- High growth in the U.S. Expansion continued across the U.S., which posted 8% rent growth. Infill markets continued to outperform areas with fewer barriers to supply.

- Acceleration in Europe. Rental growth escalated to 5%, a break from the recent 2-3% that had characterized the last several years, as growth broadened on the continent, led by a roll down in concessions and increases in headline rates.

- Top growth in China. Multiple factors coalesced to drive rent growth of 8%, showcasing the potential for outsized growth as China’s megalopolises increasingly become infill markets and customers find the need to adopt Class-A space.

- Considerable increases in the cost to build new facilities. This factor is clearly influencing rental rates across the globe.

Four global themes are aligning:

- Low vacancy. Around the world, vacancy rates are low (many near record levels), particularly for infill submarkets.

- Strong demand. Customer requirements continue to grow amid positive cyclical and structural drivers.

- Greater willingness to pay for quality space. E-commerce, the need to be close to consumers, and rising consumer expectations around speed and product availability are pushing a mandate for quality.

- High development cost increases across all aspects of the project. This includes land, labour, materials and pricing from general contractors and subcontractors.

Underperformance was broadly attributable to two themes:

- Weak/soft economic trends. Uncertainty stemming from geopolitics, such as NAFTA trade negotiations, subdued activity in those economies.

- Exposure to excess supply. Pockets of excess supply in certain submarkets such as Atlanta, Central Pennsylvania, the Chicago I-80 corridor, Houston, Chongqing in West China and Osaka, Japan have limited rent growth.

What's next for 2019?

Operating conditions are solid, and structural drivers for demand and development economics suggest another year of healthy growth. Of note, Europe appears poised to lead rent growth, as pent-up pricing power is accelerating rent growth on the continent. However, downside global risks include macroeconomic headwinds that could subdue sentiment. Nevertheless, should volatility increase in the general environment, structural drivers will become a more apparent support to growth.

Key themes for 2019 include the following:

- Uncertainty and volatility from the macroeconomic environment. Though far from broad-based, some economic indicators have softened and warrant caution. Uncertainty (e.g., Brexit and U.S.-China frictions) reduces expectations, which could reduce growth.

- Low availability of product. Vacancies in many markets are at or near historic lows and are likely to remain low in the near term. Customer sentiment appears to be forward-looking, focusing on long-term expansion plans.

- Replacement costs are rising. Rents for new buildings are still catching up with the rapid growth in development costs over the past few years, forming an important tailwind for the coming year.

- Location and quality are increasingly important. Building selection is vital to both supply chain efficiency and access to labour, and customers are more mindful of this in light of Last Touch® requirements.

- Barriers to supply. Markets with land scarcity will continue to outperform regional averages. Those markets include New York, Los Angeles, Beijing in North China, Hamburg and Lyon.

What does it mean for customers?

In an era of increased competition, logistics customers with thorough planning processes and a forward-thinking mentality that enables them to act quickly will secure the best real estate at the best prices. Particularly in infill areas, vacancy rates were low and replacement costs rose. At the same time, the importance of proximity to the urban consumer for faster delivery continued to grow. Supply chain evolution and fundamentals suggest that these trends will persist. Logistics planning with an end-to-end view on supply chains must factor in the value of time as a function of distance to consumers. The closer to the end consumer, the better. We expect that rents will continue to rise in 2019—even if at a slower pace.

What does it mean for investors?

Valuations in fast-moving markets can be challenging, and they require a deep knowledge of local markets. Structural drivers should underpin growth. Yet, there will be some instances of outperformance. Location is a more important factor than ever in investment decisions. Markets with high barriers to supply and those serving urban cores will find a steady flow of requirements from both business expansion plans and reassessment of supply chain strategies. Such markets should enjoy long-term forecasts of low vacancies and rent growth.