Building construction markets of the Balkan EECFA countries as a whole have shown resistance during the pandemic so far. Nonetheless, the region is foreseen to have yet another negative year in 2021, before expansion can return in 2022. The EECFA (Eastern European Construction Forecasting Association) has released its Construction Forecast Report for winter 2020.

Building construction markets of the Balkan EECFA countries as a whole have shown resistance during the pandemic so far. Nonetheless, the region is foreseen to have yet another negative year in 2021, before expansion can return in 2022. As the current EU programming period is nearing its end, civil engineering is expected to be the driving force in the upcoming period, well outperforming building construction. The total construction market is projected to side move in 2021, and 2022 could bring growth of around 4%. Based on its priorities, the NextGenerationEU recovery fund is also supportive for both building construction and the civil engineering sub-markets. Its specifics (for what and when) on the country level are yet unknown, though.

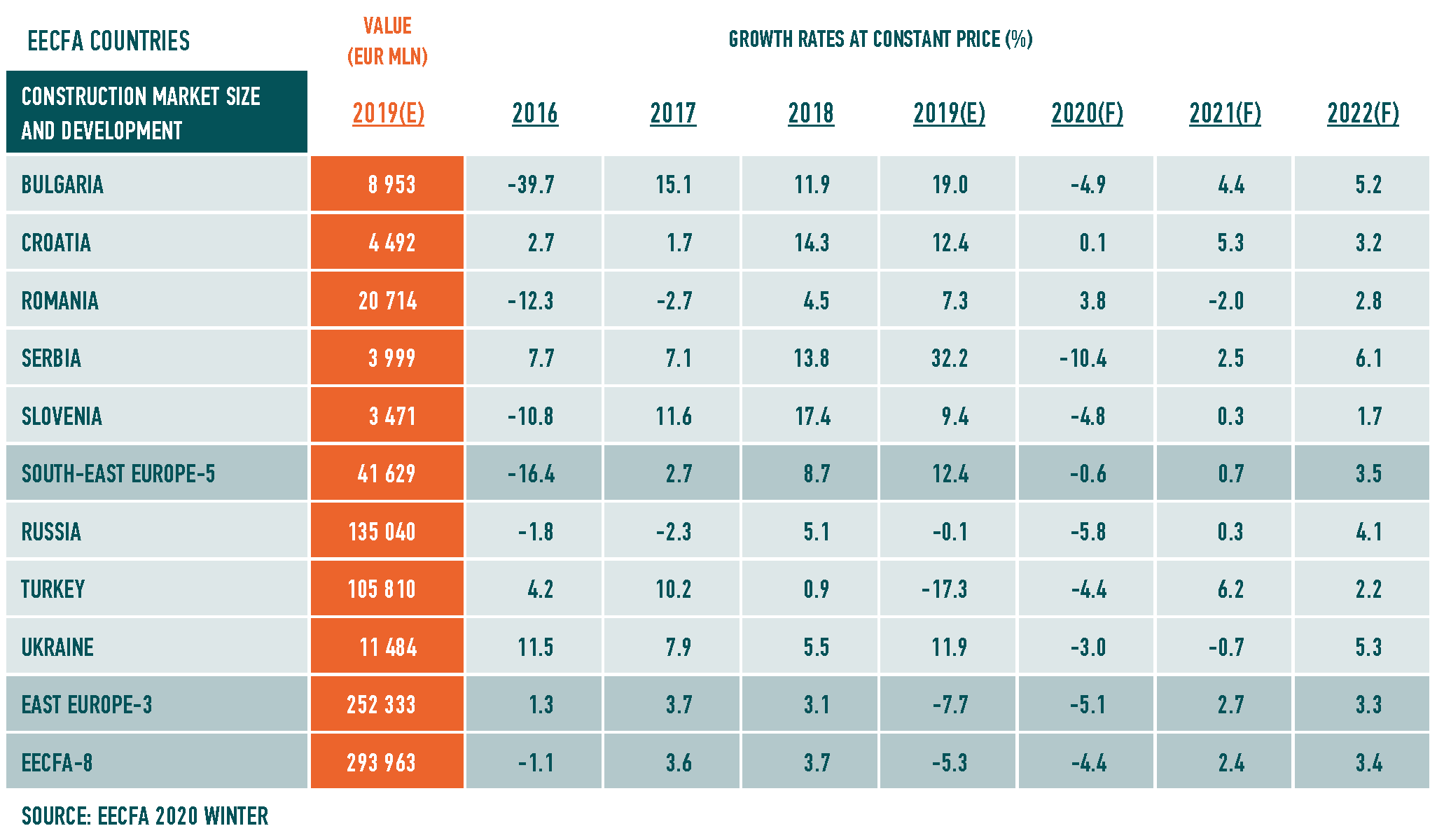

Bulgaria. The expected economic recovery should bring the Bulgarian economy back to pre-crisis levels by end 2022 with both exports and consumption contributing positively. Having it in mind, the future of residential construction remains positive despite the economic uncertainty. In short term, purchasing power should be affected, but in general, demand for new housing projects in big cities should remain. Non-residential construction will also be held back by dropping demand for commercial and hotel projects, and the projected slow and uneven economic recovery. Civil engineering in the future should be driven by EU funding as well as by the national budget. After major growth in total construction output in 2019 (+19%), 2020 will likely see a drop of 4.9%. Approaching the end of the programming period in 2021 and 2022, total construction will likely increase by 4.4% and 5.2%, respectably, in real terms.

Croatia. The effects of COVID-19 and the Zagreb earthquake on the Croatian construction industry will vary greatly from sector to sector. Thanks to swift, massive EU financial assistance, some sectors will even benefit from the disasters. These sectors include civil engineering generally and especially those CE sectors in which projects can be implemented rapidly. For buildings sectors, results are mixed. Some were harshly battered and will take years to recover. Others barely felt the catastrophes’ consequences. With few exceptions, the trends that underlay buildings sectors’ growth before these events will remain the primary drivers of buildings output in the medium and long run. In the short term, disaster-relief spending will benefit some.

Romania. Pandemic impact on construction was felt less strongly in 2020 since ongoing projects were not halted and thus the market slightly grew (3.8%). With the entire economy taking a few years to recover after the 2020 crisis, total construction output in Romania should drop in 2021 (-2%) and start recovering in 2022 (+2.8%). The pandemic will water down the housing subsector next year as fewer-than-expected new projects began this year and the recession should also continue to reduce purchasing power. In non-residential, retail and hotel were battered most. Office construction is in hiatus due to lower demand for new construction with the expansion of work-at-home scheme and with businesses rethinking the use of traditional offices. The drop in international trade set back industrial construction, but as borders open and exports start picking up, recovery may come too. Civil engineering is the brightest spot with an estimated growth in government investment as 60% of the EU funding for infrastructure is still unspent from the 2014-2020 budget.

Serbia. The developments in 2020 are marked by the reoccurring pandemic and during the year, movement restrictions were introduced twice, having a very negative effect on all service sectors. Furthermore, it is now certain that pandemic effects are to extend into 2021 and the best-case scenario means the economy will take the entire 2021 to recover. With still large uncertainty looming for next year, the forecast still carries a lot “ifs” and the government spent over 10% of GDP for various stimulus measures aiming to mitigate the effects of the interruptions. While the recovery in the second half of 2020 was strong, the new restrictions in October and December again impacted developments and stopped the normalization. Luckily, the realization of big public infrastructure projects has been steady and growing, which has helped growth in construction outputs, and private investments are still not subsiding. Strong credit activity and market fundamentals are also supporting recovery, but lingering foreign demand and slow recovery in the service sectors continue to dim the prospects.

Slovenia. The construction industry was less disrupted by COVID-19 that some were fearing. Even though construction output is estimated to have dropped by 4.8% this year, it will likely rebound next year close to the 2019 level and should expand further in 2022 on the back of civil engineering where big projects are continuing apace. The Second Railway Track to Port Koper, the Third Axis Road construction and the Karavanke Tunnel expansion all continued in 2020 and were less disrupted by the lockdown than expected. Non-residential construction, on the other hand, will suffer from the lingering effects of the economic slowdown caused by the pandemic and the consequent lower investment in industrial and commercial segments. Similarly, residential construction is subdued for the time being due to the pandemic but may return to growth path towards the end of the forecast horizon based on historically low interest rates and good availability of credit financing.