In Q3 the modern retail market in Poland grew by nearly 140,000 sqm of GLA. This is a significant increase as compared to the first half of the year when only a mere 26,000 sqm of GLA within 5 schemes were completed. Notably, the first IKEA store was delivered in Lublin with the residents of Poland’s eastern regions in mind. According to BNP Paribas Real Estate Poland, the end of the year is set to bring more than 200,000 of GLA sqm in new retail projects.

Towards agglomerations

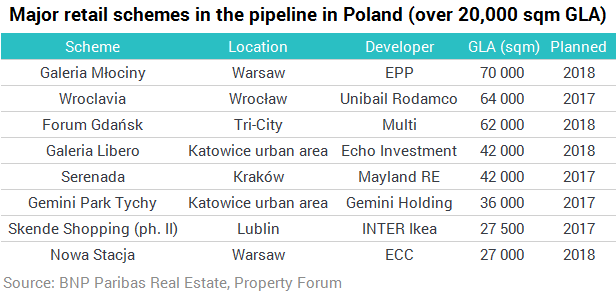

Nearly 75% of the 660,000 sqm of retail GLA currently under construction and in the process of being extended is located in the main agglomerations. The Warsaw metropolitan area is the largest and most dynamically growing market scheduled to be enriched within the next 18 months with approximately 160,000 sqm of GLA. The coming quarters will be all about the intense development of Warsaw’s northern areas with competition between Galeria Północna opened in October and Galeria Młociny, the retail and leisure complex with an additional office function with a total of 75,000 sqm of GLA currently under construction.

“According to market sources, more than 65,000 people took part in the events surrounding the opening of Galeria Północna, while one million shoppers visited the newly opened shopping centre within less than 4 weeks. This is the best testimony as to how eagerly awaited this place was and how popular it is amongst the residents of Białołęka and the north-east parts of Warsaw as well as those from the areas outside of the capital. It has to be noted that another large scheme with convenient transport links and located in close proximity to the Młociny node will open very soon, i.e. Q1 2019,” said Natasa Mika, Director, Retail Department at BNP Paribas Real Estate Poland.

Strong end of the year

By the end of the year developers are set to deliver to the market another 200,000 sqm of retail GLA. The key completions of Q4 took place first in the capital of Lower Silesia where Unibal-Rodamco opened its Wroclavia complex, while a week later Kraków saw the inauguration of Serenada with its 160 stores on which construction commenced in the autumn of 2015. Work and preparations are currently under way in respect of opening of the Skende shopping centre next to the IKEA store in Lublin. The completion of this important retail destination for the entire region is planned for the second half of November. The authors of the report stress that a significant part of the new stock scheduled to be opened towards the end of the year will come in the shape of small retail schemes, mostly retail parks and strip malls in large cities and small regional markets.

“Over the first three quarters of the year the value recorded for retail investment was at a level of €1.3 billion, which at the same time accounted for more than a half of the total volume of transactions concluded on the commercial market. There is a new trend to be noticed amongst investors, which is their increased willingness to locate their capital in retail formats other than traditional shopping centres. Retail park and outlet centre portfolio acquisitions had a high share in the total retail transaction volume,” commented Patrycja Dzikowska, Head of Research and Consultancy at BNP Paribas Real Estate Poland.

As a result of the transactions scheduled to complete in Q4 2017, this year's transaction volume might significantly exceed the value recorded at the end of last year.

Minimum increase as regards vacancy rate

Between January and June the vacancy rate for shopping centres increased by 0.6 p.p. and at the end of H1 it reached 4.1%. This slight increase resulted from the closing down of Praktiker stores across Poland. It has to be stressed that as far as the analysed period is concerned, clear disparities in vacancy rates for prime retail destinations and secondary schemes became more apparent. The most vacant space is available in Katowice (5.9%) and Kraków (5.4%), while it would be more difficult to find vacancies in the Tricity (3.1%) and Warsaw (2.6%).