The European construction industry will be hit hard by the COVID-19 crisis, according to Euroconstruct's latest forecast for 19 European member states.

Abrupt downturn in 2020, recovery to come in 2021

There will be an abrupt downturn in the European construction markets this year, but a slow recovery will begin already next year. As these markets had a lot of challenges already upfront the COVID-19 crisis with stagnation trends in many countries, it is not surprising that the ongoing crisis will have a huge negative impact on the markets in all Euroconstruct countries this year. But – as the national experts of Euroconstruct foresee it right now – there will be a positive return already next year and normalisation in 2022. Compared to the 2019 levels, we will - despite the expected upturn and normalisation in 2022 – lose at least €300 billion in total output from 2020 to 2022. As per the new Euroconstruct forecast, the number of total unemployed persons will increase from 15.3 million in 2019 to 20.5 million this year. And approximately 1.5 million of this growth in unemployment will be caused by the activity drop in the construction sector.

Results from last year

In 2019, total construction output in the Euroconstruct area (19 European countries) grew by 2.9% compared to 2018. New construction (including new residential, non-residential, and new civil engineering buildings) had been driving the market for several years, and increased by 3.9% last year, while renovations have been growing steadily at around 2%. Total construction output reached about €1,700 billion in 2019, and during the winter report (November 2019) the market was anticipated to decrease its growth rate to around 1% annually over the next two years as a result of a weakening economy.

COVID-19 impact

Nevertheless, the world has changed dramatically since the appearance of the novel coronavirus. As of now, the forecast for 2020 has been revised downwards with more than 12 percentage points, indicating a decline of 11.5%. This drop in construction is similar in size to the decline caused by the global financial crisis in 2009. Total construction output is expected to reach about €1,500 billion, corresponding to the level of 2015, hence, losing several years of growth. However, total construction for the Euroconstruct area will see a rebound already next year of around 6% and then continue to grow by 3% in 2022, reaching an output level similar to the one in 2018. Still, there are downward risks to the forecast, the most significant being the coronavirus and its containment. Questions such as will there be further lockdowns after restrictions are being eased, or will everyday life start to go back to normal after the summer, are affecting the market view. The uncertainty in the development of the virus and its effects on the economy is very high.

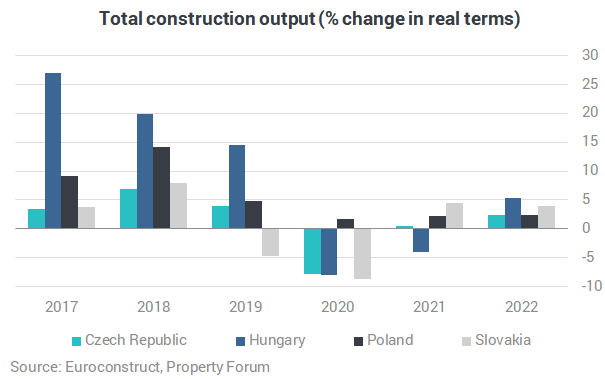

Not all countries are negative

All but a few of the 19 countries of the Euroconstruct area are seeing a decline in 2020, where the UK and Ireland are predicting to have the largest drop of around 33% and 38%, respectively. At the same time, Finland and Switzerland are expecting smaller drops in total construction, approximately by 1%-2%. On the other hand, Portugal and Poland are expecting continuing growth during the crisis, indicating that there is a fragmented view among the countries on the impacts of the coronavirus. Among the “Big five” countries, it is only Germany that will see a small decrease (-2.4 %) in total construction this year, while the rest (France, Italy, Spain and the UK) are expecting to have a decline between 12% and 33%. Although all countries are expected to rebound in 2021 and 2022, the magnitude of growth will be smaller than the fall in 2020.

How subsectors will perform

The different subsectors of construction are all affected by the crisis, but some more than others. For the 19 countries of the Euroconstruct area, the least affected subsector is civil engineering, which is expected to decrease by 7.2% this year and then to recover in 2021 and 2022 with a growth of 7.4% and 3.5%, respectively. Both residential and non-residential constructions are set to fall by more than 12% in 2020 and then start to improve from next year and the year after, between 3%-6% annually.