The investment volume achieved in 2016 totalled almost €1.2 billion with 46 transactions recorded in core CEE hotel investment markets. In comparison, 2015 reached just over €700 million with 45 transactions. Austria was the star performer with almost €800 million transacted, which made up 67% of the total investment volume. In other CEE markets volume was lower than in 2015 with a particular decline in Poland which more than halved in volume. The Czech Republic accounted for 18% of total CEE investment share; most of the investment took place in Prague which saw 7 transactions including the Hilton Old Town, Park Hotel and Chopin Hotel.

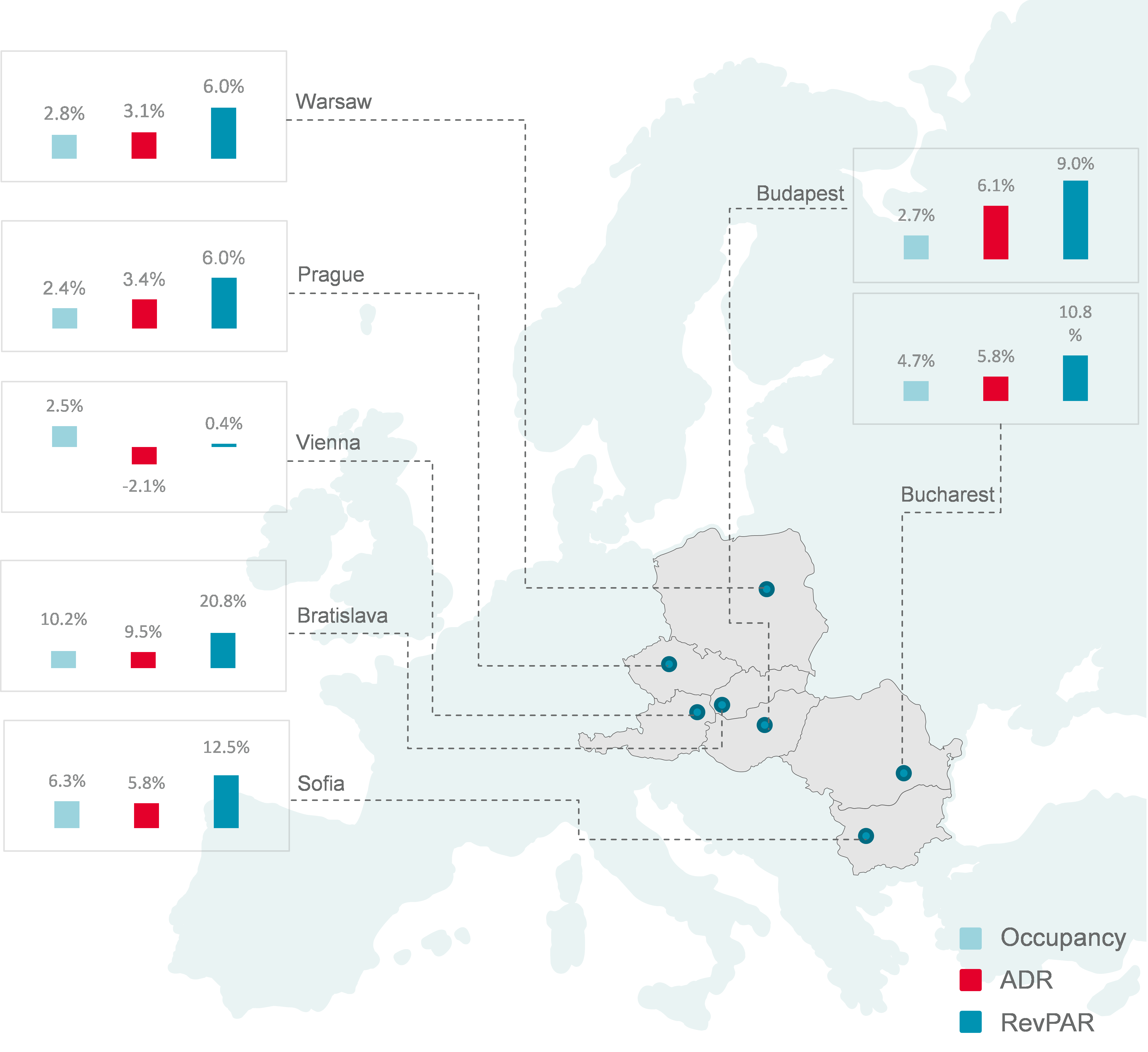

The CEE hotel industry reported growth across all key performance metrics. Increasing number of tourists have chosen CEE destinations, thus occupancy rates returned or even surpassed the pre-crisis levels, reaching 72% on average up from 69%. As the cost of visiting CEE has gone up along with the increasing hotel room rates, profits have been soaring. The average price per room reached €76.6 up from €73.6 in 2015. While the Eastern markets achieved double digit growth in terms of revenue per available room, the more mature markets of Central Europe including Prague and Warsaw saw growth of around 6%.

Performance change over 2016

Money has been flowing in from Far East Asia, the Middle East, America as well as Europe. Hence the region has become truly international.

“In the last few years the region has seen important inflows of capital as wider groups of investors try to take advantage of the strong performance of the local hotel industry. Among the key factors driving performance are the continued strength of inbound international tourism into the CEE region, supported by Asian travellers as well as the re-focus of North African and Western European tourism. Moreover the willingness of banks to finance hotel acquisitions has significantly enticed high investor demand,” says David Nath, Head of CEE Hospitality Team at Cushman & Wakefield.

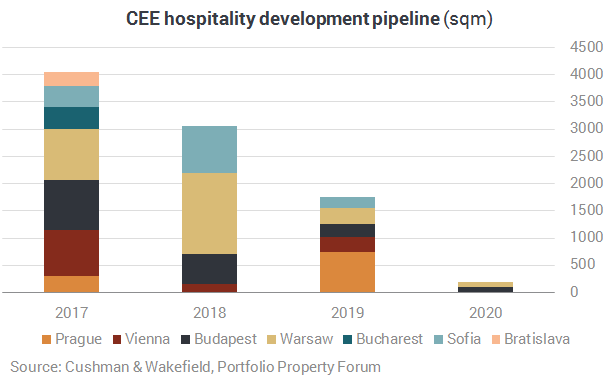

Banks’ appetite for lending is reflected in the return in hotel development activity with 2017 expected to deliver an additional 4,000 rooms across Central and Eastern European capital cities. The markets with the greatest development prospects are Warsaw and Budapest. Prague is an exception with a limited pipeline due to planning constraints and only a few sites suitable for hotel development.

“Although we expect growth to slow down slightly, during 2017, the investment market will remain robust compared to other more established markets in Western Europe. We will also see increasing capital invested in less mature hotel investment markets such as Bucharest and Sofia” says Frederic Le Fichoux, Head of Hotel Transactions - Continental Europe and adds “Average daily rate is expected to rise further, generating higher income returns for investors especially in more mature CEE markets, where the development pipeline is limited.”

In 2017, investors’ activity will be notable especially in Hungarian, Austrian and Romanian hotel investment markets, where significant assets are set to be put up for sale or about to be transacted.

UDH, one of Poland’s largest distributors of premium imported beers, has leased approximately 1,400 sq m of modern warehouse and office space at the Park Rysy Kraków distribution centre. The tenant, which has chosen to expand its operations in southern Poland, was once again represented by AXI IMMO.

Golden Star Estate has secured a long-term lease agreement with global technology solutions and consulting provider C&F for nearly 1,900 sqm of office space at the Konstruktorska Business Center. Following the transaction, the property, located in Warsaw’s Mokotów business district, is now almost fully leased. The Polish branch of C&F will officially relocate to the facility at the beginning of 2027.

Natland Group has committed to its long-term presence at Prague-based Rohan Business Center through a lease extension covering 2,004 sqm of office space, together with storage facilities and dedicated parking spaces, in a deal brokered by iO Partners.

New appointments

Indotek Group has announced the appointment of Diederik Bakker as Group Chief Investment Officer and Group Head of Asset Management. In his new role, the Dutch real estate investment professional will gradually assume responsibility for the company's ITAM (investment, transaction, and asset management) activities across 12 European countries, supporting the next phase of Indotek Group’s growth. His focus includes facilitating sound investment decisions across Europe and developing a group-level portfolio management strategy that combines local market knowledge with international asset management know-how.

Peakside Capital Advisors has appointed Bogi Gabrovic to advise the board and support its investment and acquisition activities in Poland. Gabrovic brings more than 25 years of CEE real estate experience to the role, having previously held senior executive positions at CTP, Golub & Company, and White Star Real Estate, where she managed transactions exceeding €2 billion.

Katarína Brydone, Jana Vlková and Vendula Maršová have been appointed as the first Equity Partners of Colliers’ Czech business. Brydone brings more than 20 years of experience in international real estate. Vlková has more than 25 years of experience in commercial real estate. Maršová, Partner and Head of Valuation and Advisory Services, brings more than 16 years of experience in real estate valuation and advisory.

On 6 August, Warsaw's Monta Beach Volley Club will host the 15th JLL Charitable Beach Volleyball Tournament of the Real Estate Industry. Running under the motto "Family stays together," this year's event will raise funds for the daily operations of the Ronald McDonald House at the Institute "Memorial – Centre of Child Health" in Warsaw. The house, which opened to families in May, offers 20 family rooms and round-the-clock communal spaces, allowing parents to stay close to their hospitalised children free of charge. The annual cost of maintaining one room is approximately 90,000 PLN. Property Forum is a proud Media Partner of the event.

CTP has signed a long-term lease with Quick Service Logistics (QSL) for a 10,658 sqm built-to-suit distribution centre at CTPark Budapest Vecsés. The facility will include more than 10,100 sqm of frozen, chilled and ambient storage space, plus over 500 sqm of offices, and is expected to be completed in October 2026.

The Polish Chamber of Commercial Real Estate (PINK) has published office market figures for eight major regional markets in Poland (Kraków, Wrocław, the Tri-City, Katowice, Poznań, Łódź, Lublin, Szczecin) for Q2 2026. The data, sourced from advisory companies including Avison Young, CBRE, Colliers, Cushman & Wakefield, JLL and others, covers existing stock, new completions, take-up and vacancy rates.

Property Forum is a leading event hub in the CEE real estate industry with over 10 years of experience. We organise conferences, business breakfasts and workshops focused on real estate, in London, Vienna, Warsaw, Budapest, Bucharest, Bratislava, Prague, Zagreb and Sofia, amongst other locations.

I have read the Privacy Policy of International Property Network Inc. and I consent to International Property Network Inc. sending me newsletters and managing my personal data provided for this purpose.